WORKING CAPITAL MANAGEMENT: CONCEPT, IMPORTANCE AND OBJECTS

WORKING CAPITAL MANAGEMENT: CONCEPT, IMPORTANCE AND OBJECTS

·

INTRODUCTION

The present research seeks to study in depth

the Working Capital Management of selected paper companies in India

A number of companies for the past few years

have been finding it difficult to solve the increasing problems of adopting

seriously the management of working capital. Business concerns intent on

developing their business have to use to the utmost, their available resources

for the improvement and development of the business there by enabling them to

increase their profits. Working Capital and change in working capital,

especially in inventories, which is one of the components of working capital form

a very important part of the total gross-capital formation in the paper

companies. Efficient and the optimal utilization of fixed assets is very

closely related to the proper management of working capital. The present

research attempts to recognize initially the importance of working capital as a

part of the total capital. It further

goals to recognize the factors influencing the working capital, its volume, and

in the process try to suggest remedial measures which might help in optimizing

the use of working capital. It also

considers as to how precisely “financing working capital” and further more what

should be mix of different components of working capital.

Some important questions to which the research attempts to seek answer as

follows:-

·

Whether paper companies have planted their

working capital requirement properly.

·

Have the paper companies utilized the

investment in current assets?

·

Have the paper companies controlled and

utilized cash resources effectively and profitably?

·

Whether paper companies resort to high build

up of inventory.

·

How far have the paper companies been

successful in collecting their `different

administration of its various components: like as inventory, account

receivable, cash, and accounts payables.

Working Capital is the life blood of every

business concern. Business firm cannot make progress without adequate working

capital. Inadequate working capital means shortage of inputs, whereas excess of

it leads to extra cost. So the quantum of working capital in every business

firm should be neither more nor less than what is actually required. The

management has to see that funds invested as working capital in their

organization earn return at least as much as they would have earned return if

it invested anywhere else. At the time of increasing capital costs and scare

funds, the area of working capital management assumes added importance as it

deeply influences a firm's liquidity and profitability. A notable feature of

utilization of funds is that they are of recurring nature. Therefore, efficient

working capital management requires a proper balance between generation and

utilization of these funds without which either shortage of funds will cause

obstruction in the smoother functioning of the organization or excess funds

will prevent the firm from conducting its business efficiently. So the main

objective of working capital management is to arrange the needed funds on the

right time from the right source and for the right period, so that a tradeoff

between liquidity and profitability may be achieved.

A firm may exist without making profits but

cannot survive without liquidity. The function of working capital management

organization is similar that of heart in a human body. Also it is an important

function of financial management. The financial manager must determine the

satisfactory level of working capital funds and also the optimum mix of current

assets and current liabilities. He must ensure that the appropriate sources of

funds are used to finance working capital and should also see that short term

obligation of the business are met well in time.

·

DEFINITIONS OF WORKING CAPITAL

Definitions of Working Capital, as per various management

experts are as under:

“Working Capital is the excess of C.A.

- H.G, Guthmann “Working Capital is descriptive of that capital which is not fixed. But the

more common use of the Working Capital is to consider it as the difference

between the book value of the C.A. and current liabilities.”

- Hoglend. J. Bierman, and A. K. Mc Adams,.

“Working Capital represents the excess of C.A.

- J.L. Brown and L.R. Housard.

“Working Capital to a firm’s investment in

short term assets cash short term securities, accounts, receivables and

inventories.”

-Weston the Brigham

“Working Capital represents only the current capital

assets.”

- Meal Baker Malott and Field.

“Working Capital means a sum of C.A”

“A Working Capital deficit exits if current

liabilities exceed C.A.”

-Prof. C.W. Gerstoberg.55

“Working Capital equals the aggregate value

of C.A.

- Lincoln

“Gross Working Capital may be used to refer

to total C.A. and net

working capital refers to the surplus of C.A.

- Prof. S.C. Kuchhal

·

CONCEPT OF WORKING CAPITAL MANAGEMENT

There are two concepts of working capital viz

.quantitative and qualitative. Some people also define the two

concepts as gross concept and net concept.

According to quantitative concept, the amount

of working capital refers to ‘total of current assets’. What we call current

assets? Smith called, ‘circulating capital’. Current assets are considered to

be gross working capital in this concept.

The qualitative concept gives an idea

regarding source of financing capital. According to qualitative concept the

amount of working capital refers to “excess of current assets over current

liabilities.” L.J. Guthmann defined working capital as “the portion of a firm’s

current assets which are financed from long–term funds.”

The excess of current assets over current

liabilities is termed as ‘Net working capital’. In this concept “Net working

capital” represents the amount of current assets which would remain if all

current liabilities were paid. Both the concepts of working capital have their

own points of importance. “If the objectives is to measure the size and extent

to which current assets are being used, ‘Gross concept’ is useful; whereas in

evaluating the liquidity position of an undertaking ‘Net concept’ becomes

pertinent and preferable.It is necessary to understand the meaning of current

assets and current liabilities for learning the meaning of working capital,

which is explained below.

Current assets – It is rightly observed that “Current assets have

a short life span. These type of assets are engaged in current operation of a

business and normally used for short– term operations of the firm during an

accounting period i.e. within twelve months. The two important characteristics

of such assets are, (i) short life span, and (ii) swift transformation into

other form of assets. Cash balance may be held idle for a week or two; account

receivable may have a life span of 30 to 60 days, and inventories may be held

for 30 to 100 days.”Fitzgerald defined current assets as, “cash and other

assets which are expected to be converted in to cash in the ordinary course of

business within one year or within such longer period as constitutes the normal

operating cycle of a business.”

Current liabilities – The firm creates a Current Liability towards creditors (sellers) from whom

it has purchased raw materials on credit. This liability is also known as

accounts payable and shown in the balance sheet till the payment has been made

to the creditors. The claims or obligations which are normally expected to

mature for payment within an accounting cycle are known as current liabilities.

These can be defined as “those liabilities where liquidation is reasonably

expected to require the use of existing

resources properly classifiable as current assets, or the creation of other

current assets, or the creation of other current liabilities.”

·

CIRCULATION SYSTEM OF WORKING CAPITAL

Working capital is also known as ‘circulating

capital or current capital’ Kulkarni has remarked that, “The use of the term

circulating capital instead of working capital indicates that its flow is

circular in nature”.

Figure – 1.1 Circulation System of Working Capital

The funds in a business are obtained from the

issue of share, the issue of debentures, and other long-term arrangement and

from operations of business. A huge part of generated funds is used to acquire

fixed assets, viz, plant and machinery, land building and some other fixed

assets, while the remaining part of the generated funds is used for day to day

operations of the business e.g. to pay wages and overheads expenses for the raw

materials processed. This makes possible the stocking of finished goods by

whose sales either accounts receivables are created or cash is received. In

this process profits are generated. A part of the profit is used to pay tax,

interest and dividends, while the remaining part is ploughed back in the

business. The circulation system of working capital may be depicted as shown in

figure 1.1 as Above page page. The cycle goes constantly throughout the life of business.

·

TYPES OF WORKING CAPITAL

Following diagram clear the classification of

working capital Accoding to the needs of business, the working capital may be

classified into following two basis:

·

On the basis of periodicity

·

On the basis of concept

Figure -1.2 Types of Working Capital

·

On the basis of periodicity:

The requirements of working capital are

continuous. More working capital is required in a particular season or the peck

period of business activity. On the basis of periodicity working capital can be

divided under two categories as under:

·

Permanent working capital

·

Variable working capital

This type of working capital is known as Fixed

Working Capital. Permanent working capital means the part of working

capital which is permanently locked up in the current assets to carry out the

business smoothly. The minimum amount of current assets which is required to

conduct the business smoothly during the year is called permanent working

capital. For example, investments required to maintain the minimum stock of raw

materials or to cash balance. The amount of permanent working capital depends

upon the size and growth of company. Fixed working capital can further be

divided into two categories as under:

·

Regular Working capital:

Minimum amount of working capital required to

keep the primary circulation. Some amount of cash is necessary for the payment

of wages, salaries etc.

·

Reserve Margin Working capital:

Additional working capital may also be

required for contingencies that may arise any time. The reserve working capital

is the excess of capital over the needs of the regular working capital is kept

aside as reserve for contingencies, such as strike, business depression etc.

·

Variable or Temporary Working Capital:

The term variable working capital refers that

the level of working capital is temporary and fluctuating. Variable working

capital may change from one assets to another and changes with the increase or

decrease in the volume of business.

The variable working capital may also be

subdivided into following two sub-groups.

·

Seasonal Variable Working capital:

Seasonal working capital is the additional

amount which is required during the active business seasons of the year. Raw

materials like raw-cotton or jute or sugarcane are purchased in particular

season. The industry has to borrow funds for short period.

It is particularly suited to a business of a

seasonal nature. In short, seasonal working capital is required to meet the

seasonal liquidity of the business.

·

Special variable working capital:

Additional working capital may also be needed

to provide additional current assets to meet the unexpected events or special

operations such as extensive marketing campaigns or carrying of special job etc.

Difference Between Permanent and Variable Working

Capital:

The distinction between permenent or fixed working

capital and variable working capital or temporary working capital is of great

importance in operating cycle and raising the funds. However, there is always a

minimum level of current assets which is contiuously required by the firm to

carry on its business operations. This minimum level of current assets is

refered to as permenent or fixed working capital and is permanent in the same

way as the firm’s fixed asset.

Permanent and Temporary Working Capital

Depending on the chang in production and sales, the need

of working capital, over and above the permenent working capital, will

fluctuate.

For example, extra inventory of finished good will have

to be maintained to support the peak periods of sale and investment in

receivables may also increse during the period. Both the kinds of working

capital-permenent and temporary –are necessary to facilitate production and

sale through the operating cycle, but temporary working capital is created

by the firm to meet liquidity requriments that will last only

temporarily. In above figuire shows the diference between permentt and

temporary working capital.

It is sh-own in below figure that permenant working

capital is stable over time, while temporary working capital is

fluctuating-some times incrasing and sometimes decrasing. However, the

permanent working capital line need not be horizonltal if the firm’s requriment

for permenent capital is incrasing or decreasing over period. For a growing

firm, the difference between permanent and temporary working capital can be

depicted

2) On the basis of concept:

on the basis of concept working capital is divided into

two categoties as under:

(A) Gross Working Capital:

Gross working capital refers to total

investment in current assets. The current assets employed in business give the

idia about the utilization of working capital and idia about the economic

postion of the company. Thus, gross working capital the amount of funds

invested in different current assets. Gross working capital concepts is popular

and acceptable concept in the field of finance.

(B) Net Working Capital:

Net working capital means current assets

minus current liabilities. The difference between current assets and current

liabilites is called the net working capital. If the net working capital is

positive business is able to meet its current liabilites. Net working capital

concept provides the mesasurement for determining the creditworthiness of

compny.

·

FACTORS DETERMINING OF WORKING CAPITAL

Papers, with their fixed investment, appear to have the

lowest requirement for current assets. This does not mean that the problem of

working capital may be minimized in this field of enterprise, since ready funds

are still essential to cover disbursement for wages, interest on funds debt,

purchase of materials and supplies, etc. indeed, under such conditions the

working capital position may become even more strategic in character because of

its relation to, and control of the large amount of fixed assets. Thus, one of

the outstanding problems of paper management in recent years has been the

maintenance of current position sufficiently strong to permit vigorous

operations. Public utilities, like the paper, have a fixed investment which

causes the current assets to constitute only a relatively small percentage of

the total assets. There is a difference between operating and holding

companies, but even then the funds required to cover current transactions are

minor as compared with those necessary to finance the long term structure.

Industrial companies, generally, require a large amount

of working capital although it various from business to business of lack of

uniformity characterizing each field of enterprise. However, the underlying

determinants of the amounts of fixed capital are required for operation;

working assets may be expected to occupy

a smaller niche in the assets structure. For similar reasons, a rapid

turnover of capital will inevitably mean a large proportion of current assets. In the

case of industries with fixed

investment, one of the primary uses of working capital is its conversion into

operating plant structure. In turn, it is expected that the income resized form

operations will normally replace such defections. This means that the flow of a

portion of working capital is circulating through fixed investment that its

recovery is dependent upon the income realized. Where the current assets are relatively more

important, a rapid sales turnover is usually found.

Often, as a case of retail concerns, the specific working assets constitute the

object of sale and recovery is direct and immediate. In manufacturing enterprises, a large share of working capital

management is more likely to become charged in form by conversion into finished

products, but even here, the potentiality of recovery is not delayed as long as

in the case of public utilities and paper companies. The need for working

capital varies with changes in the volume of business. A considerable

proportion of current assets is needed permanently as fixed assets. More than

one production cycle may be in process at one and the same time, for business

operations on a continuing basis. Materials are purchase and work is in

progress. Finished inventory is sold. At the same time new receivables

accumulate and old ones are converted into cash. Cash is utilized in the

production process.

The following factor determine the amount of working

capital

·

Nature of

Companies:

The composition of an asset is a function of

the size of a business and the companies to which it belongs. Small companies

have smaller proportions of cash, receivables and inventory than large

corporation. This difference becomes more marked in large corporations. A

public utility, for example, mostly employs fixed assets in its operations,

while a merchandising department depends generally on inventory and receivable.

Needs for working capital are thus determined by the nature of an enterprise.

·

Demand of Creditors:

Creditors are interested in the security of

loans. They want their obligations to be sufficiently covered. They want the

amount of security in assets which are greater than the liability.

·

Cash Requirements:

Cash is one of the current assets which are

essential for the successful operations of the production cycle. Cash should

not adequate and properly utilized. It would be wasteful to hold excessive

cash. A minimum level of cash is always required to keep the operations going.

Adequate cash is also required to maintain good credit relation. Richards Osbom

has pointed out that cash has a universal liquidity and acceptability. Unlike

illiquid assets, its value is clear- cut and defines.

·

Nature and Size of Business:

The working capital requirements of a firm are basically

influenced by the nature of its business. Trading and financial firms have a

very less investment in fixed assets, but require a large sum of money to be

invested in working capital. Retail stores, for example, must carry large

stocks of a variety of goods to satisfy the varied and continues demand of

their customers. Some manufacturing business, such as tobacco manufacturing and

construction firms also have to invest substantially in working capital and a

nominal amount in the fixed assets. In contrast, public utilities have a very

limited need for working capital and have to invest abundantly in fixed assets.

Their working capital requirements and nominal because they have cash sales

only and supply services, not product. Thus, no funds will be tied up in

debtors and inventories. The working capital needs of most of the manufacturing

concerns fall between the two extreme requirements of trading firms and public

utilities. Such concerns have to make adequate investment in current assets

depending upon the total assets structure and other variables. The size of

business also has an important impact on its working capital needs. Size may me

measured in terms of the scale of operation. A firm with larger scale of

operation will need more working capital than a small firm.

·

Time:

The level of working capital depends upon the time

required to manufacturing goods. If the time is longer, the size of working

capital is great. Moreover, the amount of working capital depends upon

inventory turnover and the unit cost of the goods that are sold. The greater

this cost, the bigger is the amount of working capital.

·

Volume of

Sales:

This is the most important factor affecting the size and

components of working capital. A firm maintains current assets because they are

needed to support the operational activities which result in sales. They volume

of sales and the size of the working capital are directly related to each

other. As the volume of sales increase

in the investment of working capital-in the cost of operations, in inventories

and receivables.

·

Terms of Purchases and Sales:

If the credit terms of purchases are more favorable and

those of sales liberal, less cash will be invested in inventory. With more

favorable credit terms, working capital requirements can be reduced. A firm

gets more time for payment to creditors or suppliers. A firm which enjoys

greater credit with banks needs less working capital.

·

Inventory

Turnover:

If the inventory turnover is high, the working capital

requirements will be low. With better inventory control, a firm is able to

reduce its working capital requirements. While attempting this, it should

determine the minimum level of stock which it will have to maintain throughout

the period of its operations.

·

Receivable

Turnover:

It is necessary to have an effective control of

receivables. A prompt collection of receivables and good facilities for setting

payable results into low working capital requirements.

·

Business Cycle:

Business expands during periods of prosperity and

declines during the period of depression. Consequently, more working capital

required during periods of prosperity and less during the periods of

depression. During marked upswings of activity, there is usually a need for

larger amounts of capital to cover the leg between collection and increased

sales and to finance purchases of additional materials to support growing

business activity. Moreover, during the recovery and prosperity phase of the

business cycle, prices of raw materials and wages tend to rise and require

additional funds to carry even the same physical volume of business. In the

downswing of the cycle, there may be a brief period when collection

difficulties and declining sales together cause embarrassment by the resulting

failure to replenish cash. Later, as the depression runs its course, the

concern may find that it has a larger amount of working capital on hand than

current business volume may justify.

·

Value of Current Assets:

Decreases in the real value of current assets as compared

to their book value reduced the size of the working capital. If the real value

of current assets increases, there is an increase in working capital.

·

Variations in Sales:

A seasonal business requires the maximum amount of

working capital for a relatively short period of time.

·

Production

Cycle:

The time taken to convert raw materials into finished

products is referred to as the production cycle or operating cycle. The longer

the production cycle, the greater is the requirements of the working capital.

An utmost care should be taken to shorten the period of the production cycle in

order to minimize working capital requirements.

·

Credit Control:

Credit control includes such factors as the volume of

credit sales, the terms of credit sales, the collection policy, etc. with a

sound credit control policy, it is possible for a firm to improve in cash

inflow.

·

Liquidity and Profitability:

If a firm desires to take a greater risk for bigger gains

or losses, it reduces the size of its working capital in relation to its sales.

If it is interested in improving its liquidity, it increase the level of its

working capital. However, this policy is likely to result in a reduction of the

sales volume, and therefore, of profitability. A firm, therefore, should choose

between liquidity and profitability and decide about its working capital

requirements accordingly.

·

Inflation:

As a result of inflation, size of the working capital is

increased in order to make it easier for a firm to achieve a better cash

inflow. To some extent, this factor may be compensated by the rise in selling

price during inflation.

·

Seasonal Fluctuations:

Seasonal fluctuations in sales affect the level of

variable working capital. Often, the demand for products may be of a seasonal

nature. Yet inventories have got to be purchased during certain seasons only.

The size of the working capital in one period may, therefore, be bigger than

that in another.

·

Profit Planning and Control:

The level of working capital is decided by the management

in accordance with its policy of profit planning and control. Adequate profit

assists in the generation of cash. It makes it possible for the management to

plough back a part of its earnings in the business and substantially build up

internal financial resources. A firm has to plan for taxation payments, which

are an important part of working capital management. Often the dividend policy

of a corporation may depend upon the amount of cash available to it.

·

Repayment

Ability:

A firm’s repayment ability determines level of its

working capital. The usual practices of a firm are to prepare cash flow

projections according to its plans of repayment and to fix working capital

levels accordingly.

·

Cash Reserves:

It would be necessary for a firm to maintain some cash

reserve to enable it to meet contingent disbursements. This would provide a

buffer against abrupt shortages in cash flows.

·

Operational and Financial Efficiency:

Working capital turnover is improved with a better

operational and financial efficiency of a firm. With a greater working capital

turnover, it may be able to reduce its working capital requirements.

·

Change in Technology:

Technological developments related to the production

process have a sharp impact on the need for working capital.

·

Firm’s Policies:

These affect the level of permanent and variable working

capital. Changing in credit policy, production policy, etc are bound to affect

the size of working capital.

·

Activities of the Firms:

A firm’s stocking on heavy inventory or selling on easy

credit terms calls for a higher level of working capital for it than for

selling services or making Cash sales.

·

Attitude of Risk:

The greater the amount of working capital, the lower is

the risk of liquidity.

`Whenever there is current strain, it has to be

immediately diagnosed on the basis of the red signals which manifest themselves

in the operations. The restrictions expressed as ratios of the elements of

current assets and current liabilities are frequently referred to as current

position constraints and include the current ratio, the acid test ratio, and

the so-called “compensating balance” ratio. Contracts with fund suppliers

frequently provide for current-position constraints.

If stock not moving fast, and if there is an excess

inventory buildup corrective steps should be taken to sell the stock or bring

down its level.

If the receivable have become sticky, effective recovery

steps should be taken to reduce the debts and to increase the collections. If

the strain is allowed to continue because of involvement in any other business

or industry, the consequences may be disastrous. In such situation, the ability

to meet current demands deteriorates; short term credits are not forthcoming;

production is affected; sales decline; cash flow decline; income may disappear;

and the whole enterprise may get into the red over a period of time. All the

above points are the factors determining working capital management in all the

companies. Some factors are controlled and some factor are not controlled by

the management.

·

OPERATING CYCLE

The duration of time required to complete the sequence of

events right from purchase of raw material / goods for cash to the realization

of sales in cash is called the operating cycle, working capital cycle or cash cycle.

This cycle can be said to be at the heart of the need for

working capital. In the words of O.M. Joy: “The operating cycle refers to the

length of time necessary to complete the following cycle of events.”

The above operating cycle in figure relates to a

manufacturing firm where cash is needs to purchase raw materials and convert

raw materials into work-in-process is converted into finished goods. Finished

goods will be sold for cash or credit and ultimately debtors will be realized.

The non-manufacturing firms, such as whole sellers and

retailers, will not have the manufacturing phase; they will have rather direct

conversion of cash into finished stock, into accounts receivables and then into

cash. The operating cycle of a non manufacturing firm is shown as under.

The non-manufacturing firms, such as whole sellers and

retailers, will not have the

manufacturing phase; they will have rather direct conversion of cash into

finished stock, into accounts receivables and then into cash. The operating

cycle of a non manufacturing firm is shown as

under.

In addition to this, some service and financial concerns

may not have any inventory at all. Suchc firm have the shortes operating cycle

as shown in figure-1.7 as next page.

Operating

Cycle of Service and Financial Firms

A working capital term loan (WCTL) should

process specific characteristic as laid down below:

·

Working capital term loan is a shortage

“long-term surplus” or net working capital(NWC) in a unit that a bank chooses

to fund.

·

It is a long term need of the unit that is

met by the bank though its short term port-folio.

·

Working capital term loan may be either clean

or secured depending upon the margin stipulated or the amount of working

capital term loan in relation to the chargeable current assts.

·

It must be repaid is a prescribed maximum

number of installments.

·

It is not sanctioned as such but segregated

out of existing outstanding, when outstanding exceed the unit’s eligibility.

·

It is a sort of ‘once-in-a-life-time’ loan. It is a post-facto corrective measure, it

should not be repeated normally.

·

It should be repayable form long-term

sources. If the repayment is form short term sources, the permissible bank

finance will fall correspondingly and working capital term loan will rise there

by neutralizing the process of repayment.

Moreover, both physical and financial follow up can be

used to complement each other, if the concept of the ‘margin’ is refined and

integrated into the maximum permissible bank finance (MPBF)

MPBF = NWC + OSCL – NCCA/CCA Margin

Where NWC is net working capital, OSCL means other

current liabilities less creditors for purchases. NCCA are non-chargeable

current assets on which no drawls are permitted. CCA means chargeable current

assets on which margin are proposed to be stipulated. The application of margin

would be coupled with the deduction of the value of creditors for purchases

from the advance value to arrive at the drawing power. Once a margin is

stipulated, it can be utilized as the operating thumb rule for monitoring the

borrower’s stake in the stocks charged to the bank as well as a rough and ready

method for keeping the drawings power within the MPBF limits.

·

ADEQUACY OF WORKING CAPITAL

N.K. Kulshrestha has observed that, “the need for

maintaining an adequate working capital can hardly be questioned. Just a

circulation of blood is very necessary in the human body to maintain life,

smooth flow of funds is very necessary to maintain the heath of the firm”.

Adequate working capital becomes necessary because of the following reasons:

·

It protects a business form the adverse

effects of shrinkage in the values of current

assets.

·

It is possible to pay all the current

obligations promptly and to take advantages of cash discounts.

·

It ensures to a greater extent the

maintenance of a company’s credit standing and provides for such emergencies as

strikes, floods, fibers, etc.

·

It permits the carrying of inventories at a

level that would enable a business to serve satisfactory the needs of its customers.

·

It enables a company to extend favorable

credit terms to customer.

·

It enable a company to operate its business

more efficiently because there is no delay in obtaining materials, etc.,

because of credit difficulties.

·

It enables a business to withstand periods of depression smoothly.

·

There may be operating losses or decreased

retained earnings.

·

There may be excessive non-operating or

extraordinary losses.

·

The management may fail to obtain funds from

other sources for the purposes of expansion.

·

There may be an unwise divided policy.

·

Current funds may be invested in non-current assets.

·

The management may fail to accumulate funds

necessary for meeting debentures on maturity.

·

There may be increasing price necessitating

bigger investments in inventories and fixed

assets.

·

EXCESS OF INADEQUACY OF WORKING CAPITAL

The firm should maintain a sound working capital

position. It should have adequate working capital to run its business

operations. Both excessive as well as inadequate working capital positions are

dangerous form the firm’s point of view. Excessive working capital means idle

funds which earn no profit for the firm. Paucity of working capital not only

impairs firm’s profitability but also results in production interruption and

inefficiencies.

When the company is inadequate, a company faces the

following problem:

·

It is not possible for it to utilize

production facilities fully for want of working capital.

·

A company may not be able to take advantages

of cash discount facilities.

·

The credit-worthiness of the company is

likely to be jeopardized because of lack of

liquidity.

·

A company may not be able to take advantages

of profitability business opportunities.

·

The modernization of equipment and even

routine repairs and maintenance facilities may be difficult to administer.

·

A company will not be able to pay its

dividends because of the non- availability of

funds.

·

A company cannot afford to increase its cash

sales and may have to restrict its activities to credit sales only.

·

A company may have to borrow funds at

exorbitant rates of interest.

·

Its low liquidity may lead to low

profitability in the same way as low profitability results in low liquidity.

·

Low liquidity would positively thirteen the

solvency of the business. A company is considered illiquid when it is not able

to pay its debts on maturity. It must be wound up under section 433 of the

companies Act, 1956, upon its inability to pay its debts.

An enlightened management should therefore, maintain an

adequate amount of working capital on a continuous basis. Sound financial and

statistical techniques by judgments should be used to predict the quantum of

working capital.

·

Commercial Bank (Bank Credit):

The major part of working capital is provided by commercial bank to their

customer. Commercial banks play an important role in providing capital to its

customers. Commercial banks are an important source of working capital in India India

Banks provided working capital in the form of cash

credit, overdraft, discounting bills of exchanges etc. banks take into account

the several factors of the borrowing concern before fixing credit limit. Bank

credit to commercial sector was Rs. 21, 23,363 crores at the end of March 200723.

There were 36,927 officers of nationalized banks at the end of March 2007.

·

OPTIMUM LEVEL OF CURRENT ASSETS

The financial manager should determine the optimum level

of current assets so that the wealth of shareholders be maximized. In fact,

optimum level for each type of current assets should be fixed. The question of

optimum investment in each type of current assets is discussed. Here we simply

discuss the basic concept involved in determining the level of current assets.

Current Assets and Fixed Asset:

A firm needs fixed and current assets to support a particular level of

output. However, to support the same level of output, the firm can have

difference levels of current asset. As the firm’s output and sales increase,

the need for current assets increase in direct proportion to output; current

assets increase at a decreasing rate with output. This relationship is based

upon the notion that it takes a greater proportional investment in current

assets when only a few units of output are produced than it does later on when

the firm can used its current assets more efficiently.

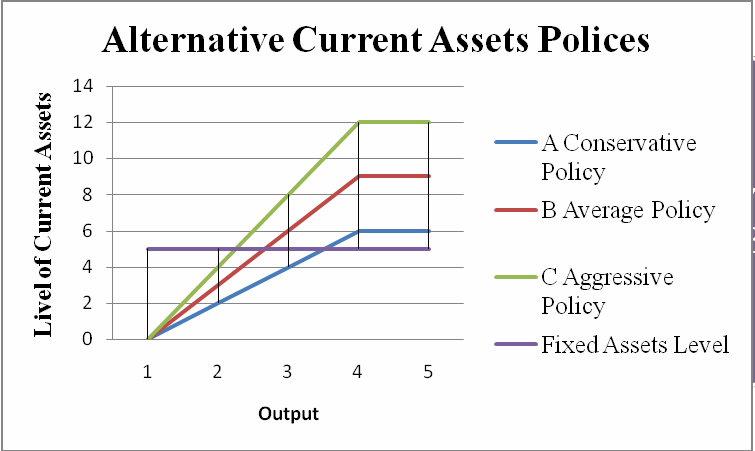

Alternative Current Assets

Polices

The help of the above graph the most

conservative policy is alternative A, where CA/FA ratio is greatest at every

level of output. Alternative C is the most aggressive policy, as CA/FA ratio is

lowest at all levels of output. Alternative B lies between the conservative and

aggressive polices and is an average policy.

Other things assuming constant, a

conservative policy implies greater liquidity and lover risk and poor

liquidity. The current assets policy of the most firms may fall between these

two extreme policies.

The level of current assets can be measured by relating

current asset to fixed assets. Dividing current assets by fixed assets gives

the CA/FA ratio. Assuming a constant level of fixed assets, a higher CA/FA

ratio indicates a conservative current assets policy, and a lover CA/FA ratio

means an aggressive current assets policy.

·

FINANCING CURRENT ASSETS

The firm must find out sources of funds to finance its

current assets. It can adopt difference financing policies. Three types of

financing be distinguished: long term financing, short-term financing and

spontaneous financing. The important sources of long term financing are shares,

debenture, preference share, retained earnings and debt form financial

institutions. Short-term financing refers to those sources of short term credit

that the firm must arrange in advance. These sources included short-term bank

loans, commercial papers and factoring receivable. The firm must find out the

sources of funds to finance its current assets. In the words of O.M. Joy: “in

comparing financing plans we should distinguish between three different kinds

of financing: long-term financing, negotiated short-term financing and

spontaneous short-term financing”. The major source of spontaneous short-term

financing is trade credit and outstanding expenses. Therefore, a firm would

like to finance its current assets with spontaneous source of the fullest

extent. Every firm is expected to utilize spontaneous sources to the fullest

extent. Thus, the real choice of financing current assets is between short-term

and long term sources. The following three important approaches are applied in

practice.

·

Matching Approach:

The firm can adopt a financial plan which involves the

matching of the expected life of assets with the expected life of the source of

funds raised to finance assets. Thus, a ten years loan may be raised to finance

a plant with an expected life of ten years; stock to be sold thirty day may be

financed with a thirty-day bank loan or

so on. Thus, when the firm follows matching approach, long-term

financing will be used to finance fixed assets and permanent current assets.

shows the firm’s investment and financing patterns over

time under a matching plan. As the firm’s fixed assets and permanent current

asset levels increase, the long term-term financing level also increases. When

temporary current assets level increase, short-term negotiated financing

increase, and when the firm has no temporary current assets, it is also has no

short-term negotiated financing.

·

Conservative

Approach:

Conservative finacing plasare those plans that use more

long-term finacing than is needed under a matching approch. The above figure-1.11

illustrates this approch. The firm is financing a protion of its temporary

current assets requriments with long-term finanging. Also, in periods when the

firm has no temporary current assets, the firm has exess finacing available

that will be invested in marketable securities.

These

plans are called conservative because they involve relatively heavy use of

long-term financing.

Figuer-1.11

·

Aggressive

Approach:

A firm may be aggressive in financing its assets. An

aggressive policy is said to befollowed by the firm when it uses more

short-term financing than warranted by the matching plan. Under an aggressive

policy, the firm finances a part of its permenent current assets with short-term

financing.

Some

exxtemely aggressive firms may even finance a part of their fixed assets with

short-term financing. The relatively more use of short-term financing makes the

firm more risky.

Thanks for sharing such an amazing information where you have given complete information about WORKING CAPITAL MANAGEMENT: CONCEPT, IMPORTANCE AND OBJECTS...Falling short of funds to run your business? Avail quick funds from our Working capital loan to meet the venture capital requirements of your business

ReplyDeleteThese days it is hard to get home loans. Either its home equity loan or its mortgage loan and availability of easy home equity loans is in full bloom. These loans are uncomplicated, tenable, easily available, very flexible and tailor-made for homeowners. The best part about all this is that almost every loan lending or financial institution offers loans at high rate but Mr Pedro offers low loan rate @ 2% rate in return of such Business loan,Personal Loan, Home Loan, Car Loan.

ReplyDeleteYou can contact Mr Pedro on pedroloanss@gmail.com

Working capital loans are a lifeline for businesses, providing essential funds for day-to-day operations. Their flexibility and accessibility make them invaluable in navigating cash flow challenges and seizing growth opportunities

ReplyDeletei learned that administration can go a long way in solving the problem of the efficient working capital management. In fact, the present research of working capital management needs special attention for the efficient working and the business. It has been often observed that the shortage of working capital leads to the failure of a business.Thanks for sharing useful Information with me and it's very helpful. Being Best CA coaching Centre in Hyderabad One of the Leading Coaching Centres in Hyderabad for Chartered Accountancy.

ReplyDeleteI learned that firm can adopt a financial plan which involves the matching of the expected life of assets with the expected life of the source of funds raised to finance assets. Thus, a ten years loan may be raised to finance a plant with an expected life of ten years.Thanks for sharing useful Information with me and it's very helpful. Being Best CA coaching Centre in bangalore One of the Leading Coaching Centres in bangalore for Chartered Accountancy.

ReplyDeleteI Learned that in comparing financing plans we should distinguish between three different kinds of financing: long-term financing, negotiated short-term financing and spontaneous short-term financing”. The major source of spontaneous short-term financing is trade credit and outstanding expenses.Thanks for sharing useful Information. Being Best CA coaching Centre in Coimbatore One of the Leading Coaching Centres in Coimbatore for Chartered Accountancy.

ReplyDelete